Beyond the Algorithm: Building Critical Thinking Skills in the Age of AI

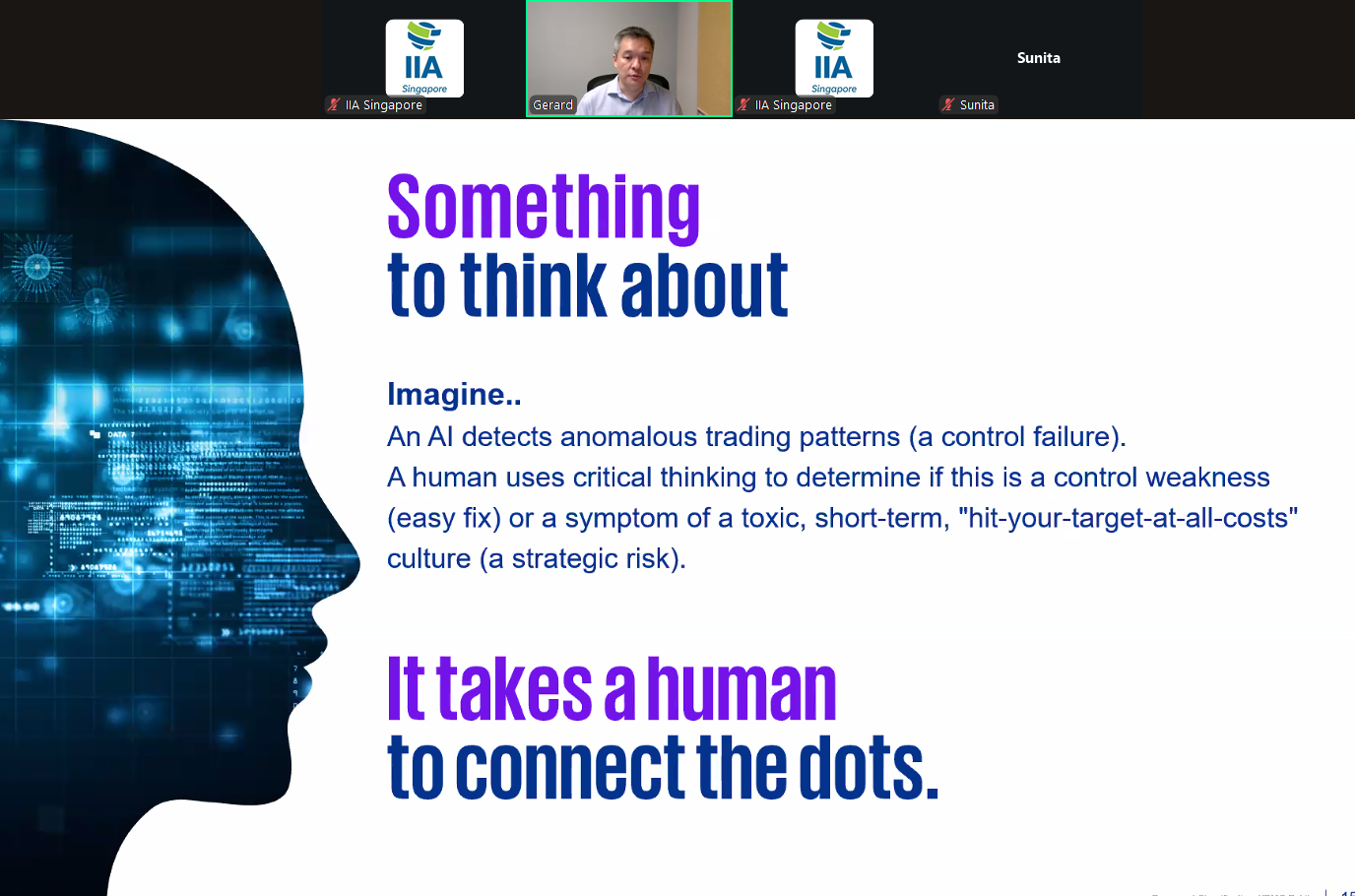

As artificial intelligence (AI) becomes increasingly embedded in audit and risk management, the webinar “Beyond the Algorithm: Building Critical Thinking Skills in the Age of AI” held on 11 November 2025 highlighted a clear takeaway that critical thinking remains the true differentiator. While AI can process vast amounts of data at lightning speed, it is the internal auditor’s ability to interpret outputs, understand organisational culture and strategic context, and weigh reputational and emerging risks that ensures insights are translated into meaningful guidance for governance and decision-making.

The speaker Gerard Toh, Partner, Risk, Advisory, KPMG in Singapore, explored how internal auditors are transitioning into new roles that go beyond traditional compliance. They are becoming ethical stewards of AI, applying judgment to interpret outputs responsibly. At the same time, they act as strategic influencers, using insights to guide decision-making rather than simply enforcing rules. They also build trust in AI-enabled systems by embedding critical thinking into audit workflows. By embracing these capabilities, internal auditors can harness technology while maintaining oversight, judgment, and professional scepticism.

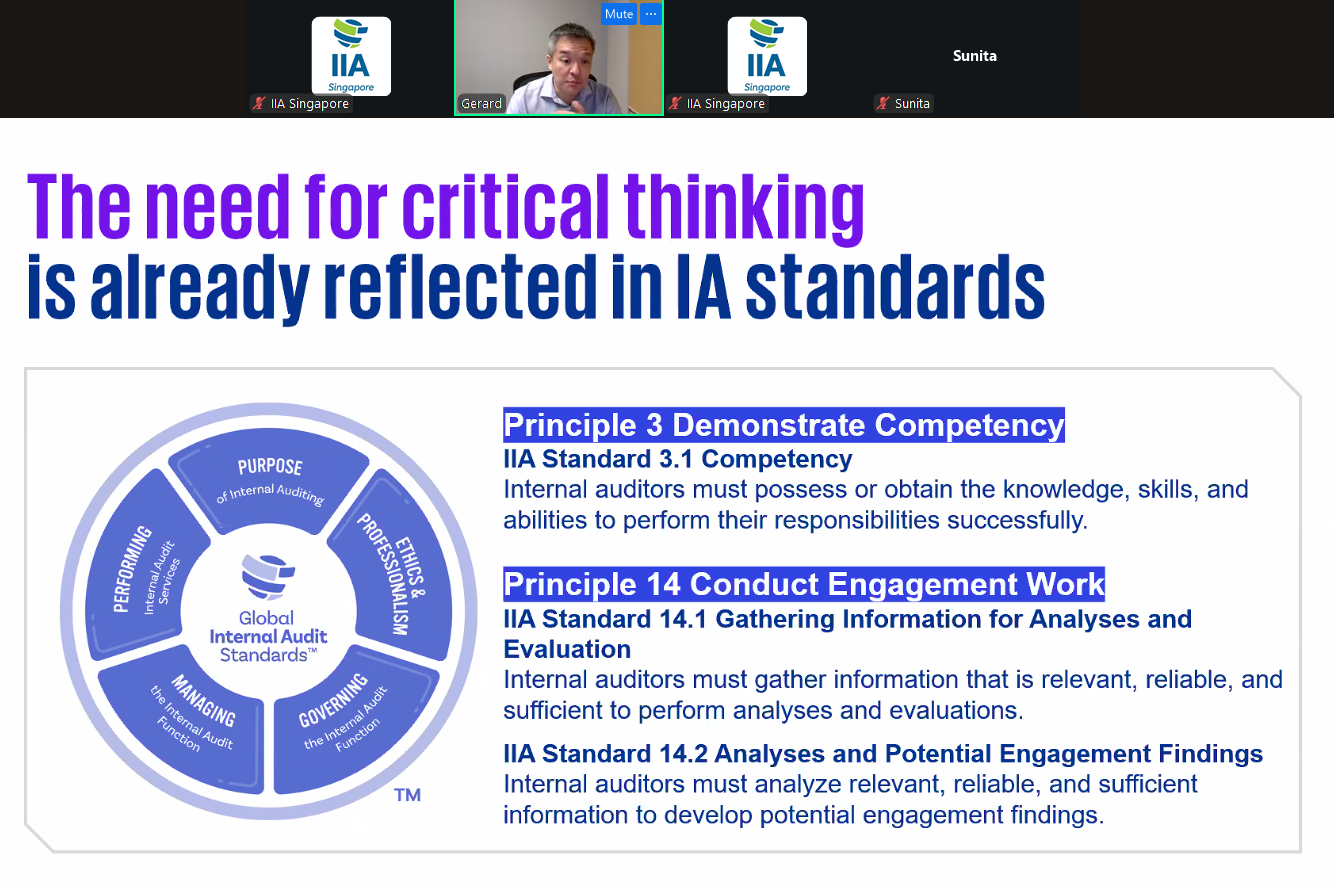

This evolution aligns with the Global Internal Audit Standards, which emphasise the knowledge, skills, and abilities required for effective internal auditing:

- Principle 3 - Demonstrate Competency

- IIA Standard 3.1 - Competency: Internal auditors must possess or obtain the knowledge, skills, and abilities to perform their responsibilities successfully.

- Principle 14 - Conduct Engagement Work

- IIA Standard 14.1 - Gathering Information for Analyses and Evaluation: Internal auditors must gather information that is relevant, reliable, and sufficient to perform analyses and evaluations.

- IIA Standard 14.2 - Analyses and Potential Engagement Findings: Internal auditors must analyse relevant, reliable, and sufficient information to develop potential engagement findings.

What sets internal auditors apart is the human edge. Their judgment and perspective show that people, not technology, are the organisation’s greatest asset in navigating complex risks.